January 15, 2025

REPORT: ‘Cash Poor’ Americans Spent $38B In Fees Beyond Loan APR Rates

“Cash poor” means having wealth in assets but insufficient liquid money available for spending and saving.

A troubling report has revealed that borrowing costs for cash-poor Americans living paycheck to paycheck are significantly higher than they expect to pay back. SoLo’s 2025 Cash Poor Report shows Americans paid more than $39 billion in fees beyond the advertised Annual Percentage Rate when borrowing money from some financial institutions to cover unplanned expenses.

According to Experian, being “cash poor” means having wealth in assets but insufficient liquid money available for spending and saving. SoLo, the only Black-owned fintech certified B Corp in the U.S. and Canada, says the figures in its report revealed a 32% increase from 2023.

What’s even more alarming in the report is that cash-poor consumers aren’t just the working class. They also represent middle-class Americans with college degrees, people who own homes, and those who consider themselves investors. Cash-poor consumers include Americans who have six-figure incomes.

“One in seven cash-poor Americans makes over $75,000 a year,” the report from SoLo reads. “Troubling trends show that nearly half of Americans living paycheck to paycheck have less than $200 In their checking and savings accounts.”

SoLo analysts, in partnership with Opinium Research, Pace University, the Global Black Economic Forum, Aspen Institute, Financial Security Program, and the Independent Women’s Forum, surveyed 2,000 American adults spanning Gen Z, millennials, Gen X, boomers, and the Silent Generation. Their data compared fees as a percentage of a $1,000 loan.

The Best and Worst Options For Cash Poor Americans, According to Report

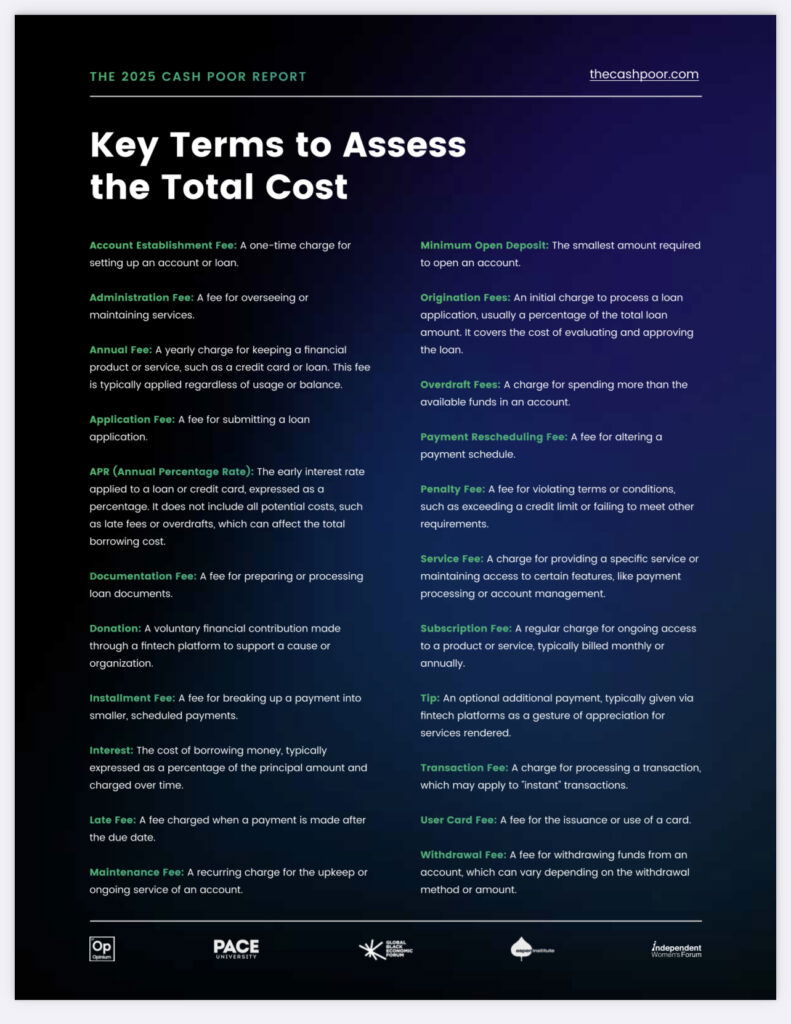

According to the report, the APR rate does not include late fees, origination fees, subscription fees, transaction fees, or other expenses that create what analysts call “debt traps” for consumers in a financial crisis.

The data shows that subprime credit cards are the most expensive option for unplanned expenses. The average cost increased to 48%, up from 41% in 2023. Because of high total fees, penalties, and monthly maintenance fees, the maximum fees can reach 90% of the principal borrowed.

“These cards account for $19.6 billion in aggregate borrowing costs in 2024, marking an $8 billion increase from last year,” according to the report.

Payday loans have the highest minimum borrowing cost among all options. Maximum costs reach 67% due to origination fees, late fees, and penalties. According to the report, aggregate costs for payday loans increased to $6.7 billion in 2024 from $6.2 billion in 2023.

Bank small-dollar loans are a relatively new offering that emerged last year. It had the third-highest costs, just behind subprime credit cards and payday loans. However, there are significant barriers to entry.

“They averaged a 25% borrowing cost this year, with a minimum fee of 12%, largely due to mandatory account balance and deposit requirements,” the report says.

Aggregate costs for bank small-dollar loans are estimated at $5.8 billion in 2024.

Earned wage access solutions offered one of the lowest average borrowing costs this past year at 13%. However, fees can rise to 26% due to optional tipping and transaction charges.

Aggregate borrowing costs for payroll advances increased to $3.8 billion in 2024, up from $3.2 billion in 2023.

Peer-to-peer loans, or P2P loans, like those offered by SoLo, remained the most affordable option regarding aggregate borrowing costs. They totaled just $1 billion in 2024, down from $1.3 billion in 2023.

Borrowing can be free for disciplined users who pay on time, but average costs due to tips and late fees can reach up to 17%.

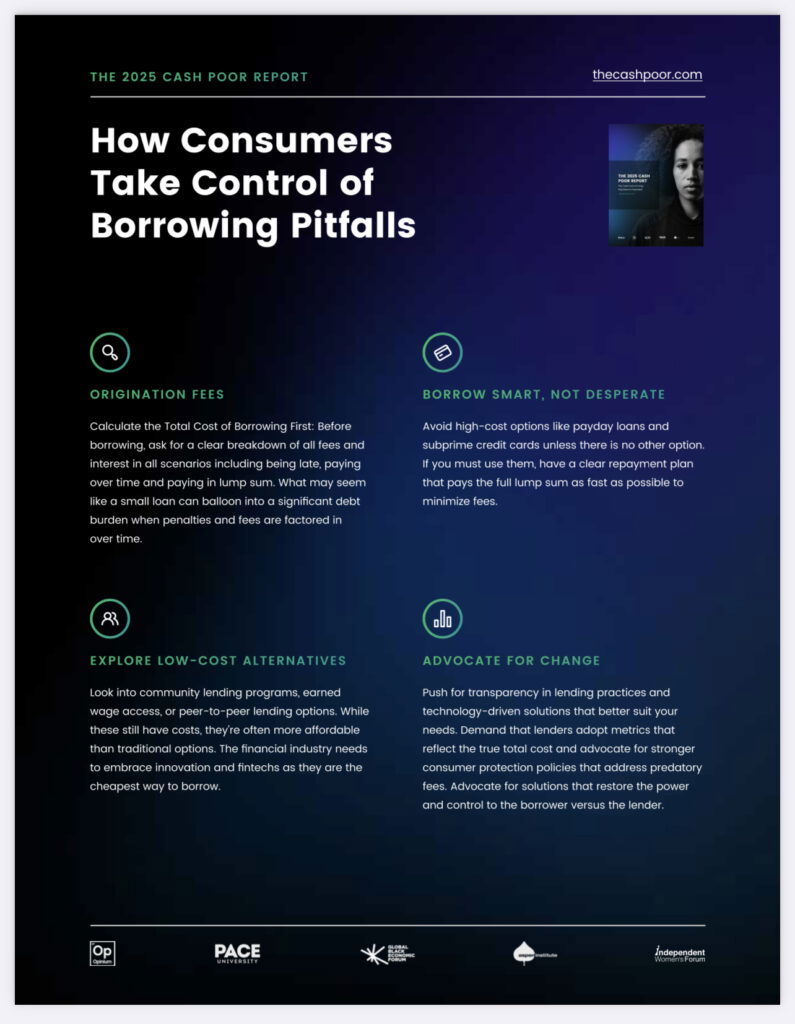

“Being cash-poor is a way of life for most Americans,” said Rodney Williams, president and co-founder of SoLo, who says this way of life creates vulnerability in managing variable and unplanned expenses.

“The vulnerability is not the time for a lack of options but rather an opportunity for innovation and competition. We want Congress and regulators to embrace innovation and allow more convenient and accessible frameworks given the same playing field as traditional financial institutions,” he adds.

Read the full report at www.theCashPoor.com

RELATED CONTENT: SNAP Increases Income Eligibility Requirements